{kind=link}

As agents, we always want the best for our clients. This would include competitive pricing, outstanding benefits and the ability to purchase these benefits from a quality company. The business owner has the same needs with a little more emphasis on price. Now the quandary: Do we offer each owner the same package (the “wants”), or do we step outside and really sell the “needs”? The following statistic should give you some insight as to the state of voluntary benefits in the workplace and how they are viewed by owners:

Approximately 20% of employers think there is value in making voluntary benefits available to their employees and only 20% list offering voluntary products as a priority in making them available to their employees!

This statistic boggles the mind.

Selling on Value, Not Price

How do we get business owners to see the value of these voluntary products? Which plans cover the wants and which plans really covers the needs? What products are we showing them? As you might guess, the top products sold as voluntary products are supplemental life and disability insurance. This is true if dental and vision plans are already provided by the employer.

What will interest the business owner? How can we get them to say, “Yes, we need this benefit.”?

Did you get the attention of a new prospect by offering the same line of goods that every other agent showed them?

You will be more likely to get the owners attention if you show a need and then fill that need.

Are the Top Voluntary Products “A Need”?

The top selling voluntary products are dental, vision, disability and supplemental life plans. All of these plans are very important and have their place; but which of these plans fill a need?

All of these products are very beneficial, but an analysis needs to be done with the business owner as to the value of the products you want to offer to their employees. We are confident that an employee and business owner would agree that the most important “need” they have is to protect their income if they are disabled and unable to work. Why not show the true value to the owner through obtaining a short term disability plan and a critical illness plan? You have now filled a need!

Critical Illness Plans: A Vital Voluntary Product

How do I get the business owners attention to add valuable voluntary products?

One idea is to show them something other than the industry norm of vision, dental, life, accident, and disability. Set yourself apart from every other agent by telling the story of Critical Illness Plans.

When a Critical Illness Plans is presented, it must be done with passion and emotion. If this is not your area of expertise, then you need to become educated as to the value of these plans.

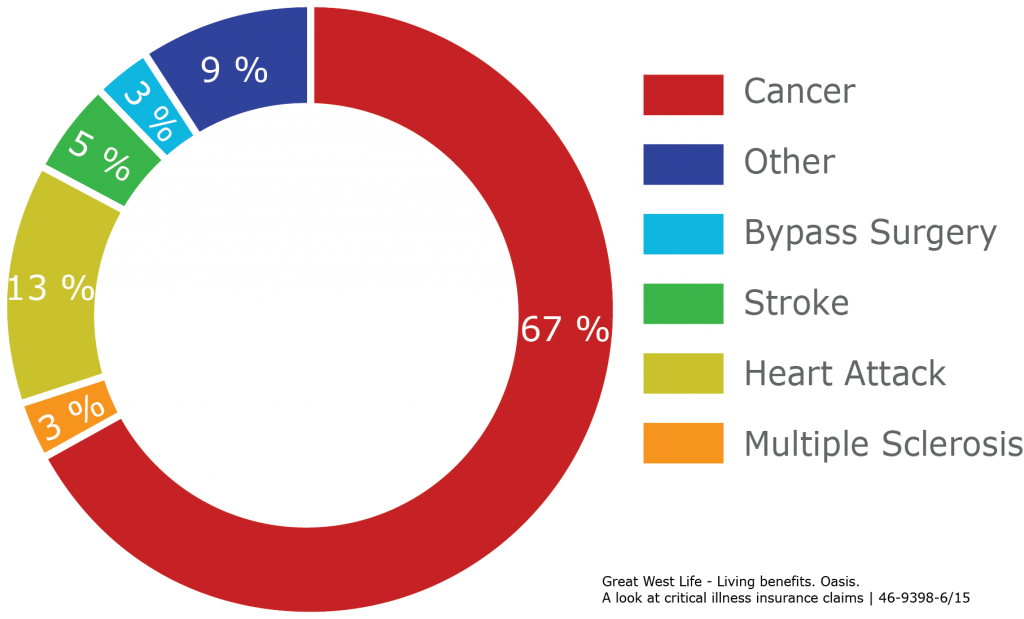

Critical Illness Insurance is needed by everyone! Most plans pay a lump sum cash benefit if diagnosed with a critical illness; such as cancer, heart attack and/or stroke.

Did you know?

While advances in medical science have significantly improved our chances of surviving heart attack, cancer, stroke or other critical illness, the fact remains that 75% of healthy individuals over age 40 will become critically ill at some time in the future. 1

For those suffering a critical illness prior to age 65, the probability of surviving is almost twice that of dying. 1

Critical Illness Awareness

I am not against vision, dental or accident products. I have to admit I have never seen a family go bankrupt due to out-of-pocket expenses from dental or vision care. Seeing how Critical Illness Plans help save thousands of families from bankruptcy, it seems almost unbelievable that these plans (CIPs) lag so far behind the others. Why is this?

Education and perception is our hypothesis. Most business owners are unaware this type of plan is available. If an owner is shown the value of this coverage, it is extremely much more likely that they will be responsive to offering this type of benefit to their employees.

Did you know that two-thirds of bankruptcies are due to medical bills and over 78% of those filing had medical insurance? 2

These plans are not a “cure-all” by any means, but there is no question that they tremendously help families in their most desperate time of financial difficulty. Many agents say they offer Critical Illness Plans as a “gap filler.” This seems like an extremely narrow and short-sighted viewpoint. Regular health insurance merely covers medical costs. What about the monthly bills, the out-of-pocket medical expenses and financial hardship due to lost income?

Employees whom have a disability plan will only receive 60% of their pay. Critical Illness Plans should be sold with a disability plan to really give full protection to employees diagnosed with a critical illness. Once you run a quote and explain the cost versus benefit, employers are bound to see that Critical Illness Plans are an extremely affordable option.

How to Determine Benefit Amount

How does one determine the amount of benefit a client needs? Agents should take the time and ask detailed questions so that they can discover the needs of their clients. One suggestion is that you determine your client’s monthly expenses; then, determine their monthly income if a situation arose where they were unable to work. It is important to note that their savings accounts should not be included in these calculations as their savings is precisely what we are trying to protect with this type of coverage.

For the benefit amount, you want to ensure that they are able to cover the deductible and co-insurance of their health plan, replace their income, and project what the medical expenses will run that will not be covered by their health plan. It is also a wise idea to project how long the individual will be unable to earn an income. These numbers will give you an idea of what the client’s total benefit amount should be.

Selling with Emotion

Critical Illness Plans need to be sold with emotion and a story. Once the appointment is set with a new prospect, you might ask what their objective is and what they think they would like to offer their employees. Smart agents listen to their clients and stand ready to compliment them on having the foresight to offer these types of plans. Ask the client why each plan they inquired about is important to them and listen carefully to their response(s). You are bound to hear that the owner wants to provide the best for his employees and help as much as he/she can.

Now is the time you should request permission to ask a couple of questions. Ask the business owner if he or she has ever had a heart attack, stroke or cancer. If they answer “no”, ask if anyone in their family or a friend has had any of those conditions. Trust me, in most cases you do not have to go beyond those folks to find they have known someone with one of those conditions. Now ask how they got through it? Did they have any financial hardships? How long before they got back to work? Did they have disability insurance?

With this information you can now present the critical illness coverage and the first person to see that need is the BUSINESS OWNER. The owner should be your first sale. Make that person the subject of the “what if” scenario. “What if you had a critical illness? Who would run the business in your absence?” Explain to the business owner that with today’s modern technology, we are more likely to survive a critical illness. Sell them on the need and how it would benefit them and you will have much better participation in enrolling the employees.

Remember, critical illness is a living benefit; it helps the living.

Selling with a Story

Some may not like this suggestion, but we believe it is the best way to present a Critical Illness product to be sold. You need a story to tell to get the point across and get the feeling out there. The most powerful story is the delivery of a claim check to a client in need. But, until you have one of these stories, you have to draw on life your personal life experiences. Try to use statistics at a minimum, but make sure that you use them to back up your story. You are trying to convey the financial hardship people experience when they are diagnosed with a Critical Illness and are unable to earn a wage.

We are confident that most of you reading this have either seen or been to a spaghetti benefit dinner for a family that is having financial difficulties due to a critical illness. This is a universal phenomenon and one most people can relate to on some level. Your solution to this problem is to offer a combination of Critical Illness coverage and disability.

We have one last comment on the delivery of a claim check. If and when this situation presents itself, it is integral that you deliver the claim-check in person. If this is impossible, it is vitally important to have a colleague deliver the check in person. You need to make every effort to have a face to face delivery. This act is often overlooked by many agents. It is all about making a personal connection. When you hand deliver a claim-check to a client in need, you have just made a friend for life. How many times are we granted that opportunity?

Set Yourself Apart from Other Agents

The Critical Illness plan should be a main offering in your basket of plans being offered and not merely an “Oh By The Way” product. Sure, it is going to take time to inform the client on the benefits of these plans; but once you are comfortable with the presentation, you will undoubtedly see an increase in referrals because you will have set yourself apart from most other agents. Will you make your clients happy by fulfilling their wants or will you make them happy by helping them fulfill their needs? Remember to be confident, sell with emotion, and speak with passion!

- 2009 Heart and Stroke Statistical Update. American Heart Association

- First National Critical Illness Risk Assessment Study published by the American Association for Critical Illness Insurance.